5G is a transformative technology, not only because of its unique attributes like slicing and low latency, or because it is the first generation of mobile technology to have a bigger impact on businesses than on consumers, but because, to really maximize its value, it can’t be treated as a standalone technology. 5G will be realized in the context of specific industries and through the co-creation of a partner ecosystem and collaboration of technologies such as AI, IoT and Edge. Effectively, 5G will need to be part of a bigger solution with a clear outcome.

This conclusion was evident in our 2020 5G market analysis, Industries and Enterprises are ready to reap the benefits of 5G, which we developed in collaboration with analyst firm Omdia. However, despite all parties coming to the same conclusion, it was clear that Communications Service Providers (CSPs) have yet to buy into that same theory. In fact, what’s worrying is that out of all 5G enterprise deals to date, only one in five early enterprise 5G deals was CSP-led, proving that the way CSPs wanted to sell was at odds with the way in which businesses wanted to buy. This year, we collaborated again with the Omdia team to review the situation a year on…

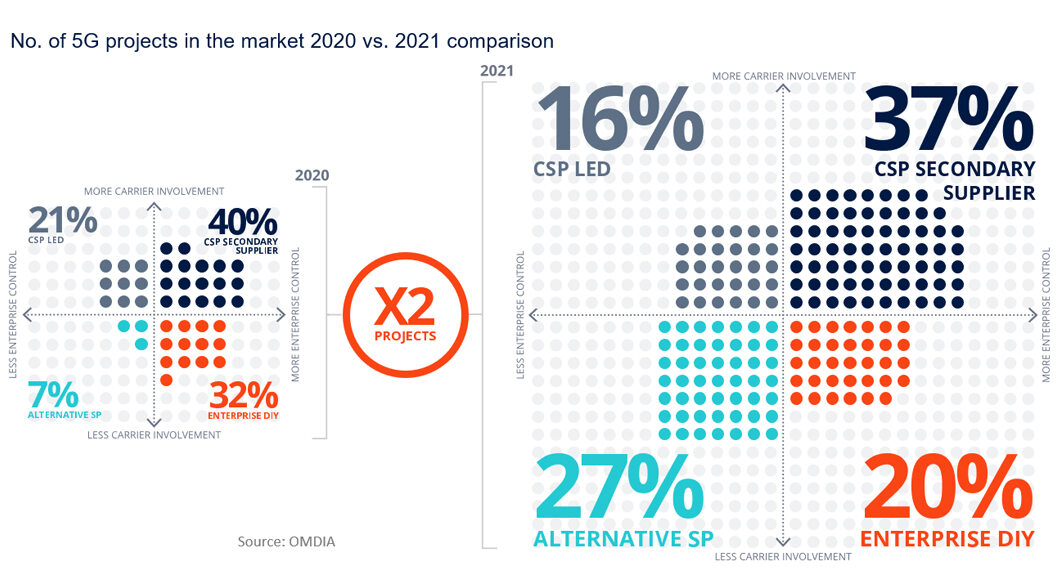

Our latest annual report one year on, reveals that telcos understand the importance of multi-technology solutions and partner ecosystem orchestration. But they are still too slow to react to enterprise demands with the share of enterprise 5G deals led by CSPs falling from 21% in 2020 to 16%.

Unlike 4G, enterprises appear to understand that 5G can be transformational for them, and they have come to this realization much faster than CSPs. As a result, the demand for 5G-led B2B solutions has doubled in the last year! Unfortunately, it seems like other players are beating CSPs to the chase when it comes to meeting this demand.

In contrast, what’s really interesting is the speed of evolution and reaction of alternative service providers such as private network specialists, who have ramped up their efforts and operations and outpaced CSPs. Their leading presence in these 5G projects has risen significantly from 7% to 27% in just a year. Edzcom is a great example as it uses a high-touch approach and has a precise vertical focus and clear market segmentation. Athonet is also disrupting the 5G market with a solution that has been adopted by major governments, public safety organizations, mines, ports, airports, enterprises and mobile operators around the world. These organizations are experts in rapidly and agilely reacting to market change and meeting customer needs through openness, partnership and commercial flexibility. And above all, they are very focused on value proposition.

Despite the headline figures, we remain optimistic about the ability of CSPs to turn the situation around. By 2022, 5G is expected to have reached viable functional maturity, and although enterprises are not hanging around, the 5G enterprise game is far from over. Many global and regional CSPs have now launched 5G enterprise services; still more now understand the need for a multi-technology, omni-partner, solution-oriented and verticalized approach for enterprise 5G. This is really encouraging.

Our study found that CSPs are starting to realize the importance of the enterprise 5G market but must fully commit and put the dedicated resources in place faster if they are to capture the opportunities as they emerge.

Overall, as an industry, CSPs need to move faster, orchestrate ecosystems and fully commit to enterprise 5G in order to capitalize on the opportunity. With the enterprise already forming ecosystems to help them address their needs, if CSPs do not formulate a strategy and invest, they will likely miss out.

The conclusion is simple: stop hesitating and commit to being more collaborative, even when you may not be in full control of the product or solution. Start living up to the expectations that enterprises and partners have of you, experimenting with business models, accelerating, testing and monetizing new offerings that are co-created with ecosystems of partners. Hopefully this will be reflected in our report next year.

I’d like to thank Evan Kirchheimer and Dario Talmesio from Omdia, a world-renowned analyst firm with a stellar reputation in the telecoms industry, for their hard work collaborating with us on this research. Right from the beginning, I was so impressed with the professionalism and extensive knowledge of these two analysts who understood the need for a deep dive into this B2B 5G conundrum.

Download your free copy of ‘CSPs readiness to reap the benefits of 5G – A year on’